Here's a "back to basics" rule that always comes in handy!

I think one of the most important keys to managing your finances is to be aware of what you are really spending money on. Think about it-- whenever people complain about being broke, don't they always say something along the lines of "I swear, I just don't know where it all goes!"

There are so many things about money that are unknowable and unpredictable. You can strategize and make educated guesses, but no one really knows what the performance of an investment will be, where interest rates will go, how tax laws will change, or whether they'll get a raise. But one thing you CAN know is what your own spending and savings habits are, and for most people, it's probably a pretty good starting place to figure out what they will be in the future, or how best to change them. Once you know what is knowable, then you can worry about the guesswork. First of all:

- Keep Records

- Look at your spending records and total them up by category.

I think a software program such as Quicken is a great investment, but you can also easily create an Excel spreadsheet or two that will serve the same purpose. Before I had Quicken, I used to do a big spreadsheet once a year. I'd sit down with my bank statements and credit card bills and enter all the transactions and sort them into broad categories. For checks and credit card expenses, it was easy to see what I had spent the money on. For cash, it was harder, but I totalled up all my ATM withdrawals and then thought about all the things I tended to buy with cash-- I multiplied out what I tended to spend on breakfast and lunch and subtracted those from the total. I subtracted an amount for laundry. Whatever was left was just categorized as miscellaneous. It wasn't very accurate, but it was a start.

Think about the categories your expenses fall into-- which ones are fixed expenses, such as a mortgage payment. Which ones are variable expenses, such as clothing? Which ones are necessities and which ones are luxuries? There is no one right way to do this-- think about what makes sense for you. Instead of just having a category for Books, for instance, you might want to have a category for Education and another for Entertainment. The cost of a book about how to start your own business might be put under Education, but a Danielle Steele novel would go under Entertainment-- you might want to think about what expenses are investments in your future in some way, vs. just throwaway spending on something with only temporary value.

- Analyze the data

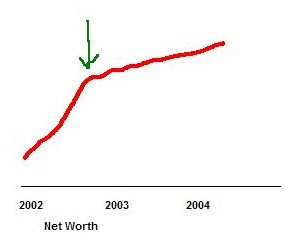

This is where Quicken can make things really fun, because of all the reports and graphs you can easily run. For example, a few years ago, I started hanging out with some new friends I'd made, who happened to enjoy good food more than some of my other friends, who I also didn't see as often. Here's a rough illustration of what I discovered:

The green arrow represents when I met those new friends, changed my social habits and started eating dinner out more often and more expensively. The shape of the red line representing my net worth is a bit exaggerated, but it just blew my mind how noticeable it was that I was saving less money just because I had started hanging out with different people! So you can bet I dropped them like a hot potato!

Ok, I'm kidding-- I did not really sacrifice my friendships on the altar of personal finance, but it did make me think we should maybe start doing some at-home dinner parties more often instead of blowing so much money at restaurants!

For other people, graphing net worth vs. friendships might be irrelevant, but if you can look at how your spending changes throughout the year, how much you spend in different categories, whether you're saving money each month or constantly in the red, you're bound to learn something about yourself. (And though analyzing your spending is a good place to start, don't forget to look at your income and investments too.) In the long run, that awareness will help you make decisions and align your actions with your priorities and goals, whatever they may be.

I suppose the reason I decided to post about this today is that I am so stressed out about what's going on with my condo purchase! I keep thinking about how much it's going to cost and trying to figure out the long-term consequences of my decisions. Sometimes it feels like I've bitten off more than I can chew, but then I remind myself that I know what I spend. I know what I have to spend and what I can cut. I know how much I save. I know where my limits are. I can do this. I'll be okay.

20 comments:

Good advice X-I'm glad you are doing the condo. I was scared to death on my first home purchase but it turned out to be a great investment. You are such a stickler for details that I'm sure it will work. Congratulations!

A very good post with lots of good advice. And just to try to be of some reassurance, you will be fine. You're doing the right thing by buying a condo. It's always scary, but in the long run, you'll be so happy you did.

It's a common emotion that all first time home buyers go through. Rest assured you'll be fine. Enjoy.

I understand EXACTLY how you feel. I'm in my house now and still feel that way. After adjusting my exemptions, and being more aware of your point #3 (analyze the data), the buyer's remorse is fading slowly.

The most important lesson I've learned to date came from a fellow blogger..."own the house, don't let it own you." That helped me to put a lot of things into perspective.

Just remember, there are more benefits to homeownership than consequences. You'll be just fine. I can't wait until your settlement day. I'm so excited for you!!

Not really sure I would want to be condo or house hunting in a market that many analysts think is on the verge of imploding. The default rate for people who bought more than they could really afford is amazingly high, if not at an all-time high. I Know it is a really difficult decision -- and that you are perhaps more financially savvy than your peers, but you might take a closer look at the idea of buying anything that has been marked up this much and is probably due for a correction. On the other hand, if you can afford it and plan to live there for many years, it probably doesn't really matter. But it could very easily be worth 20% less in a few years.

I think that tracking your expenses is actually one of the most important things you can do. I made a post about it here: http://www.intthree.com/index.php?itemid=210&catid=15 (complete with a spreadsheet that you can download). Tracking expenses allows you to make the kinds of decisions that you are currently dealing with. Can I afford this condo/house? Can I afford to retire? Can I afford this car? If it doesn't look like I can afford something, where could I shave some expenses to try to be able to afford something?

Thanks for the reminder. I am really anal about tracking my expenses, and then I tend to get burned out on it and lose track for a long time. I'm in one of those periods. I'm SIX MONTHS BEHIND in my tracking! I started to transition from Excel to Quicken around the time I started blogging (last fall) but never completed the transition. Mostly, over the last few months I've been confused about why I have so much excess money. Gotta get back on track with my budgeting so I can figure out where to stash the excess.

Just in terms of my cash spending, I've been shocked at how much less I've spent since I went on a diet in January. I'm not buying things like juice and chips as much, not to mention candy bars and ice cream. So I'm not surprised your new friendships took such a big toll.

hi there, i'm new and it sounds like you have some good ideas. it made me realize that my housing expense, of rent garden apt, electric and gas, make up 39% of my gross monthly pay. Is this bad? How much should one maximally spend in housing? How much should one maximally spend in all housing costs (mortgage, insurance, condo HOA fee, taxes,flood ins-if required)? What is the minimum or maximum amount should one save after all expenditures are considered from monthly salary? i could possibly buy a place, but all my savings would be gone in downpayment and closing, and would only have 100-300 left for saving. To me, that's scary.

Great post on tracking your spending.

I live in one of the most overpriced houseing markets in Southern California. We are not in any hurry to buy anything yet. So many people feel like they just have to "own" something or they're just throwing their money away. Then they buy houses they really can't afford with interest only adjustable rate mortgages.

A "homework assignment" that I often give my financial planning clients is to write down every dollar they spend for a month. It's often quite eye-opening.

Hi,

Do you publish on any kind of a schedule? You have one of the more interesting blogs around, but you haven't written a new blog since Wednesday, and today is Saturday. You're about to come off my favorite blogs list.

Your blog is terrible. No offense....but seriously.

Hey-here it is Sunday afternoon and I'm in Microsoft excel-monthly budget. This is painful to track everything and I blame you for making this painful but good suggestion. FYI I happen to think you have a great blog :)

I'm with Steve... what's up with the lame reader comments? Keep up the good work with your blog. You're one of the really good ones!

Nina at Queercents

I agree.

-Steven Burda

www.linkedin.com/in/burda

Your blog rocks! It's one of my best! You motivate me, an addicted spendthrift. Whoever that annonymous is just lame for real.

Your blog rocks! It's one of the best. Very simple and well-written. You definitely motivate me, an addicted spendthrift. Keep up the good work. The annonymous person is just hating. : )

Knowing yourself is the most important rule because without it you can't really answer any other questions. Maybe the scarey part is learning more about yourself. I keep all my finances tracked in my head. I'm getting killed right now in the market from knowing myself way too well. Let the ego sit on the bench and let reality check up 100% and get out into play.

Do you trade stocks/options madam x?

I was just lookin at some advice on the net for managing personal finance..coz I will be setting up a household soon...

N I found dis useful...gonna try dat...Thnx..!!

Tracking one's expenses forces honesty, and knowing you'll have to write about your bad decisions later can help prevent some of those impulse buys. My first regularly paying job was as a graduate teaching assistant. What I was paid, in upstate NY, is plenty of money for a single person, if one is careful. One does need to budget, though, and I started by tracking my expenses for a couple months. It turns out that my going out to eat "occasionally" was happening far more than occasionally.

I've recently started tracking what I eat, also. Similarly, my memory of my eating habits and the facts differ.

Humans have bad memory of their own behavior.

Post a Comment