On Thursday, I posted some spreadsheets to look at the question of whether or not you should pay points on a mortgage. A commenter rightly pointed out that my calculations did not take into account the time value of the money that you are paying in points, and said that it was never worthwhile to pay points. I've done some more math and I think I still stand by my original assertion that it may be worth it to pay points in some cases, though there are still some parts of the calculations that get a little complicated for someone like me! But here's where I am at so far:

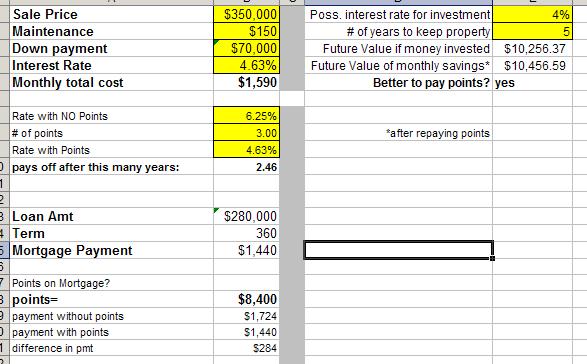

In the scenario in my previous post, I used an example of a $350k purchase price, 20% down payment, interest rate of 4.625% if paying 3 points, or 6.25% if no points. The cost of paying points is $8,400, but your monthly mortgage payment is lower by $284, and you pay less interest over the life of the loan. According to my original spreadsheet, you only had to own the property for about 2 1/2 years before the points start paying off. But that didn't take into account the interest that you might be earning if you invested the $8400.

Let's say you had that money in a bank account earning 4% interest. At the end of 3 years it would be worth about $9,469. Over 3 years you would save $284 on your payments, totalling $10,224. From that you have to recover the $8,400 you paid, so you are left with only $1,824. But of course the $284 you save each month also has time value. What if you were putting that in the same 4% interest-earning savings account every month? You still are pretty far behind-- you only have about $2,444. But after about 5 years, you are breaking even. If you're only investing the money at 4%, and you plan to own the property for at least 5 years, you may want to pay points. You can download my new spreadsheet here.

The interest rate matters-- the higher the interest you think you can earn, the longer it takes for it to be worth it to pay points. But as far as I can tell, even if you assume a 15% interest rate, you break even in only about 5.2 years. I don't know of any investments that guarantee a risk-free 15% annual return. (If you do, I would like to hear about them!) The stock market may do better than that over some time periods, but you might have ups and downs, and you could lose your money, and I believe the historical average stock market returns are lower. If you have the mortgage for 15 years, you'd have to earn an average annual return of over 40% on your money to come out ahead vs. paying points. You'd have to be a pretty savvy investor to earn that much in any given year, let alone averaging that much per year over 15 years. If you were that savvy an investor, the whole thing would probably be moot anyway, as we'd be talking about you purchasing a mansion in Greenwich, CT with cash, not paying 3 points on some crummy 2-bedroom in Brooklyn.

There are a few things this calculation doesn't take into account: I'm using the same interest rate for the lump sum investment and the monthly incremental investment-- maybe you could get a better rate on the lump sum than the small contributions. Also, the big thing I am not looking at here, because it's so complicated it's giving me a migraine, is the tax implication of each scenario. Points are fully deductible as a lump amount in the year you pay them (at least in this case), so paying points gets you a bigger tax refund that you could invest up front. Mortgage interest is tax deductible, so a higher interest rate would get you more of a tax deduction over time. But more interest is paid in the early years of the loan, so the tax deduction lessens over time. If the money is invested and produces interest, dividends or capital gains, all of those will be taxed. And for all of this, who knows what my tax bracket will be over the years that I have the loan? I'd love to hear from anyone who can help me run some calculations on all that.

The mortgage points calculator that I originally found gives somewhat different numbers from what I am calculating above. It says it takes taxes into account, but I'm not sure what other factors go into it, and though I am obviously not a math genius, I am not going to run my life by random online calculators unless I can see how they produce their numbers and be sure I think it's right. But I found another calculator on the same site that seems to come closer to my calculations, and the good news from this is that the tax implications of paying points seem to make them even more advantageous. I think I am going to email the "Mortgage Professor" to see if he'd be willing to explain it further. Conveniently enough, I'm also seeing my accountant today, so maybe I can get some more info from her for another post about the tax issues.

I also mentioned a cash flow argument in the comments on the previous post, that the higher monthly payment of not paying points would put me in the red against my budget-- I have to admit this is more of a psychological argument than a logical one. My budget doesn't take bonus or interest income into account, it's strictly a plan for spending and saving my regular paycheck cash. It also is pretty liberal in terms of including generous amounts for things like travel, etc. I didn't like the idea of having a mortgage payment that might give me a small red number on my budget spreadsheet, but in the larger scheme of things, I can "afford" the payment either way. I just don't like the idea of ever having to dip into savings at all to get past a month where expenses are a little higher than average, as opposed to being able to save a few hundred dollars every month, and put all bonus and interest income straight into savings.

So for my own situation, I still think it will probably be a good choice to pay points-- I'm buying a place that I expect to live in for several years, and my 5-10 year plan is to save enough money to buy another apartment and then rent this one out at a profit. And if my interest rate is very low, I don't see why I would refinance or sell unless some kind of emergency totally changed my situation. I see it as a choice between plans and predictable returns on the one hand, and risk and unknown events on the other.

This all illustrates to me one of the great benefits of personal finance blogging-- you talk about your decisions, people question them, you look at your reasoning again and either defend your opinions or admit you're wrong, or a little of both-- there is dialogue and it forces you to really do the math and think things through. Good stuff.

Sunday, February 26, 2006

Follow-up post on Mortgage Points

Labels:

real estate

![]()

Subscribe to:

Post Comments (Atom)

2 comments:

Madame X,

I have been watching your post on paying points with some interest. You are on the right track.

If you would like some help, I have some software that will make this all very clear and might help in your study of this on your blog. I would be happy to work with you on this if you like.

Here are some key points with points:

1.) It takes about 5 years to break even. Therefore the question is not only will you keep the home for 5 years...but will you keep the mortgage for 5 years is also a very important questions.

2.) Your assumed interest rate by paying 3 points in not realistic. Essentially, each point that you pay will get you a 1\4% reduction in rate, and the most points you are likely going to be able to pay is 4. Many lenders only offer rates with a maximum of 3 points. This all has to do with the mortgage bond that the rates are pegged to.

3.) If you are purchasing a home, rather than paying the points yourself, asking the seller to pay them. This is far more valuable to you than a reduction in the sales price.

If you would like to dialogue on any of this, I would love to help.

You are also ignoring the optionality that you are giving up by paying points. If rates drop in teh future, you gain less from this if you pay points than if you do not pay points. In fact, this is the main reason why mortgage companies give you the option to pay points!! It is pretty tough to model/value (involves ome interesting financial math) the optionality lost by paying points...

Post a Comment