[2/27/05: please read the comments and follow-up to this post!]

A commenter asks: "why the hell are you paying points?" since I mentioned that I would be doing so when buying my condo.

Excellent question! It gives me the chance to show off my dormant inner Excel geek. There's been a dearth of spreadsheets on this blog lately!

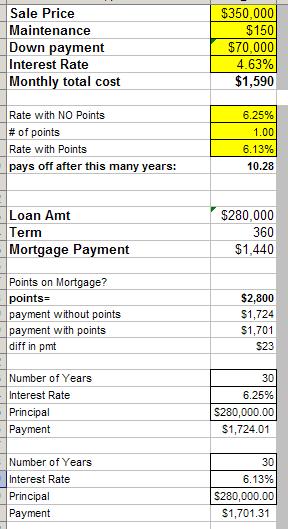

First of all, a "point" equals 1 percent of your loan amount. It's a fee that you pay up front in order to get a lower interest rate. Sometimes they are worth paying, sometimes they are not-- you have to do some calculations in each individual situation to decide what is right for you.

Here's a spreadsheet with a rough example. I set this up so I could enter the rate without paying points, the number of points, and the rate I would get if I paid those points. Then it calculates the difference between the monthly payments for each, and the dollar amount that the points will come to. More points up front get you a lower monthly payment-- you just have to figure out how many months it will take for the monthly savings to offset the upfront cost.

In this example, you might think, whoa, 3 points! What a rip-off! But if you do the math, the rate spread is large enough that the points pay for themselves in less than 3 years. If you are sure you will own the property for more than 3 years and you have the cash to pay 3 points at closing, it's worth it to lock in a really low rate on a 30-year fixed mortgage. The tidbit that is missing from this image is that over the life of the loan, you come out ahead by almost $94,000.

Here's another spreadsheet with a different example.

In this case, you're only paying 1 point. But the difference between the interest rates isn't very much, so it actually takes over 10 years for paying that point to be worth it. If you are sure you will own your home for more than 10 years, you might still want to go for it. But if it's a first home and you might sell in a few years, you might be better off just paying the higher interest rate. And over the life of the loan, you only save about $5400, so it's not that exciting.

Neither of these scenarios is my exact situation, but let's just say I'm a lot closer to the first example! In my case, I have enough cash to pay points in addition to my other closing costs. And I am pretty sure that I will live in my condo for at least a few years, and keep it to rent out even if I decide to live elsewhere. The other thing to remember is that points paid on a mortgage for a primary residence are tax deductible. For me, it was a no-brainer.

There's more info about tax deductibility at Bankrate.com. They also have some calculators but if you prefer a DIY Excel approach, you can download my spreadsheet here. Enjoy! (at your own risk, of course.)

Thursday, February 23, 2006

Why Pay Points on a Mortgage?

Labels:

real estate

![]()

Subscribe to:

Post Comments (Atom)

11 comments:

wow, i can't believe it only took you 1/2 hour to respond to that comment with this post!

You got a 30 year fixed for 4.63%?

You are my hero!!!

Hazzard

Geek OUT, girl! Seriously that was a great explanation of paying points...it's suddenly clear :)

Hazzard, that was the rate I could have gotten a few months ago. It's since gone up a bit, but is still quite low.

I like the analysis. I wished I had put more thoughts on buying down my rate 3 years ago. I would have totally made back the $$ by now.

Actually, in your example, i think the savings is more like $378 a month, since you pay off more of your principal at the lower rate. You actually break even after 22 months.

Good stuff.

yeah I'm going to have to agreed that the spreadsheet explanation is pretty straight forward and clear.

I gotta say I've read pages of and pages on points that was not clear at all.

good job!

in your first example, you would release about $8500 in cash to get a reduction of about 150 bps. you could clearly use the $8500 to earn more than three times that even in the 3 year period you think it takes to earn back the cash layout. Further, sure points are deductible, but so is interest on the mortgage, regardless of the rate, thus it makes little sense to part with cash when the interest is fully deductible. the only situation i can see where points would make sense is in a cash out refi where the mortgagor is subject to AMT. Otherwise, the time value of money dictates that parting with cash bad, investing in high yield account good. It would be wiser of you to, instead of paying the points, using the $8500 to pay down the principal after closing. the condo itslef surely will appreciate more than 150 bps in 3 yrs.

Anon, that is a good point. The other issue I should point out is one of cash flow. At least in the short term, that $2-300 difference in payments keeps me from going into the red in an average month based on my typical expenses, so it seems like if I kept the $8500, I'd sometimes be dipping into it to pay bills, as opposed to adding a little money to savings each month and feeling confident that I could invest those savings in less liquid, perhaps riskier and presumably higher-yielding ways.

But now I'm kind of itching to do another spreadsheet to figure out the minimum interest rate the money would have to make and how much I could take out of it each month and still come out ahead...hmmm.

never pay points, ever. points are a construct of the lending industry designed to dupe unwitting borrowers. if you would not be able to afford the mortgage at the prevailing interest rate, without creating a shortfall in your monthly budget, then (and I do not mean to insult you here), you should not be buying the place. I would wait it out until you can buy sans points. i'm sure the lender pushed them on you, thats their job. do not fall into that trap. thats money you will never again see. further, chances are that you either refi and/or sell out in 2-3 years and the points you paid are long gone.

I'm still not sure about the math here but using one online calculator I found, it's telling me I would have to earn over 17% on the money that would have gone to points, for a 3 year window, if the spread was 4.625 - 6.0% for 3 points.

Link to calculator

ooh, I've been thinking about this more and I'm going to have to post a followup with some more calculations! total ROI vs. annual gains, investment risk, monthly savigns being invested, lots of interesting factors so it might take me a while. my theory so far is that the anonymous commenter is right that I am at least underestimating the number of years it takes for points to pay off. For the short term, say 3 years, you could put that money in a CD and come out ahead-- but I think there may still be scenarios where if you own the the property long enough, you'd have to earn a much higher annual return on an investment than any fixed-income vehicle would offer. you get into a grey zone where you're dealing with returns that aren't guaranteed adn windows of time where future plans may be vague, etc. It's a really interesting nut to crack and I think I'll have some fun spreadsheets to post!

Post a Comment