How do you keep track of what you save? Do you stash money in a certain account and track that balance? Or do you just look at how much your net worth increases from month to month? Do you count what you save in a 401k or just cash savings?

I personally don't have a specific account designated as "savings." I have a couple of different accounts and I sometimes transfer money between them, so that method would be complicated. And looking at my net worth increases doesn't work, because I like to look at investment earnings separately from what I save out of my paycheck. My savings goals include retirement savings via my 401k and cash savings. The 401k is easy to budget-- you just set a percentage for the deductions and you're all set. But for cash, I want to be able to track how I'm doing.

For a while, I was just subtracting my expenses from my earnings each month, factoring out the 401k and considering the rest to be my savings. But that didn't factor out reimbursable business expenses, and my bonus would throw it off... and it just wasn't complicated enough for me!

I decided to create an Excel spreadsheet to summarize my expenses and income in a way that would really let me judge my actual savings. One of the reasons I wanted to do this was to make sure I wouldn't have cash flow problems after I move-- my new condo won't cost me all that much more when you factor in the tax deductions and the payments that go towards equity, but I still have to write those big checks up front, and even if I'd be saving money by year end, I wanted to see how often I might have to go into the red on certain months.

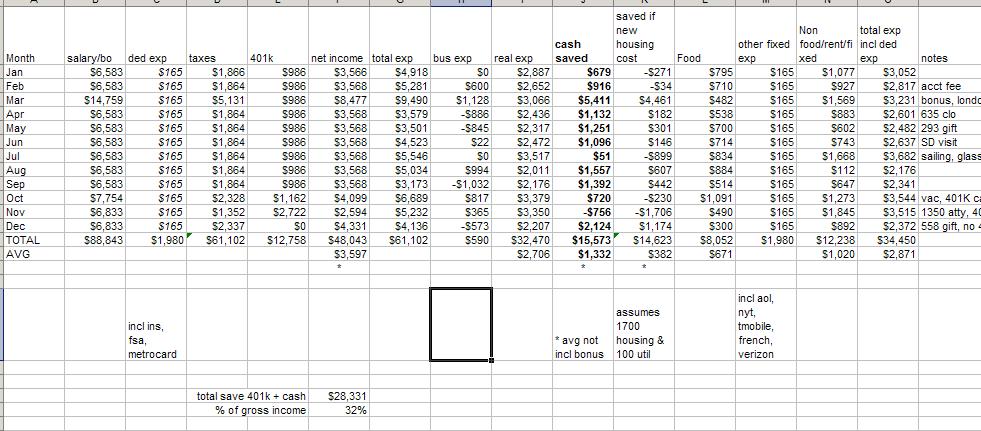

Here's a screenshot of the spreadsheet I came up with to look back at my 2005 expenses (you can download the file here if you want a better look at it, or to play around with it yourself):

Each month, I enter my gross pay minus payroll-deducted expenses (like insurance and my transit pass), minus taxes, minus 401k, to leave my net income (I could just enter my paycheck amount, but I need all the deduction info, as you'll see). Then there is a column where I enter the month's total expense amount from Quicken, and any business expense amount. The spreadsheet then subtracts the taxes and business expenses from the total expenses to give me my "real" expenses. The real expenses are subtracted from the net income to give me the amount of paycheck cash I save each month.

I then added a few more columns to play with: how much cash I would save if my housing expenses were what I'll be spending on the condo, how much my food spending was, since that is a huge item, and then how much I spent if you factor out fixed cost items such as AOL, DSL, basic monthly cost for phone, NYT subscription, rent, etc. There is a notes column so I can jot down major one-time expenses like paying my 1-year gym membership in advance, or my attorney's fee. I also have a column where the payroll-deducted expenses are added back in, since it's still money I spend.

When you factor these things out, the spending that's left is sometimes very little! In August 2005, I only spent $112 on "other" stuff beyond food, rent, and those fixed expenses. (I took a taxi, I had a bill for long-distance calls, I did laundry and bought a few things at the drugstore. That was about it! But oops, even those few things actually cost me a bit more-- I just realized it looks low because of the repayment of a loan that hit that month as a credit against an expense in a previous month. Ah the joys of accounting.) On average, my "other" expenses were about $1,000 a month in 2005, which isn't bad since it includes some big items like travel, sailing lessons, clothes, gifts, new glasses and the other large one-time expenses I mentioned above.

I added totals and averages at the bottom of most of the columns-- for the savings column averages, I always leave out March, since my bonus would skew that higher, but things still look pretty good: average net income $3,597, average expenses $2,706, average savings $1,332, or 37% of my net income. If I factor in the 401k savings and bonus, then I saved 32% of my gross income.

With my higher housing costs, I'll probably only be saving about 11% of my net income, not counting bonus and 401k. I'll also have certain months where my cash flow will be quite negative, which rarely happens now. That is a little scary to me, so I'll be trying to cut back my spending a bit to bump that savings percentage up. But when I factor in the higher tax refund I should be getting, I'll be saving over 20% of my net income by the end of the year. And if you factored in the home equity I'd be building, and any other miscellaneous interest and investment income, it would be over 30%. Even if some of that is savings I can't touch right away, I feel like I'm on track with my long term goals.

Thursday, July 13, 2006

Keeping Track of Savings

![]()

Subscribe to:

Post Comments (Atom)

5 comments:

I try to keep my savings as far from my regular money-exchanging account as possible to keep it out of my grubby little hands. So if I have money left at the end of the month, it goes into a separate account. I get paid monthly so I just start over every month. This is also an incentive to spend less money since whatever I don't spend goes into savings.

I'm not sure of your philosophy of tax refunds but I'm not one to give Uncle Sam a huge interest free loan throughout the year. You may want to use the IRS withholding calculator at: http://www.irs.gov/individuals/article/0,,id=96196,00.html

to adjust your employer's tax withholding. A little bit of information (reasonably accurate annual forecasts on taxes and interest paid) and 5 minutes of your time should get your a few extra dollars each month (helped me get ~ $200/mo) of net income which may help you in those months you forecast cash flow negative. Why wait to get the benefits of homeownership at the end of the year? Just a thought!

I started recording my balance sheets in early 90s in an Excel spreadsheet (yeah, Excel was there then). It's interesting to look back at 20+ years of my personal financial history. About 5 years ago, I started to record major expenses based upon my checkbook, which has helped me to see where all my money went.

Hi Anon 12:06-- I do plan to adjust my witholding when I'm a homeowner, but I still like to look at it as if I didn't. Just one of those psychological games to keep me in line!

Sounds like you are definately on your way to meeting your LT goals. I admire the level of tracking detail, but that takes up a lot of time. My wife and I use Quicken to track expenses. And I have also developed spreadsheets for retirement planning which basically track monthly networth and project out annual increases for the next 5 years (I think I have a pretty good idea what I can bank over the next 5 years).

I used to get into a lot of detail, but our finances are fairly complex, and it is a full time job to track in detail. Plus, we are at the point where the numbers we need to put away are fairly large, so a little rounding error doesn't hurt as long as we round down.

Plus, most of my income is in the form of bonuses, which is a blessing and a curse. Salary pays for housing expenses, ultilities, food, and entertainment. Bonus money is largely for descretionary big-ticket things. Good part is that we must carefully budget each year. We break down about 20 big ticket categories (insurance, taxes, education, travel, home improvement, etc.) and track our expenditures closely. The savings go into the investment acct from the bonus immediately, so there is no temptation. Oh, and the "curse" part about bonuses is that it's hard to predict what next year's income will be.

The only real temptation is to run a deficit in anticipation of a good year.

Our target is to save 25-30% of total annual income (excluding home equity). The purchase of our Park Slope bstone partly interrupted our savings for a couple of years, but it has been a great investment (we do get some rental income and it could be converted to a multi-unit rental property or condos in the future, so I really do consider it to be an investment in the traditional sense of the word). So, I can totally identify with some of your concerns about the months of negative cash flow you are about to experience.

With the purchase somewhat behind us, my attention has turned to building the nest egg, since the townhouse won't necessarily pay the bills when we retire. Now that I think about it, if I fully retire in 20 years (I envision a few yrs of downshifting, before full ret), the rental income will have probably kept pace with inflation and then some, and the mortgage will hopefully be paid off, so staying in the bldg might turn out to be a better proposition than I've been thinking. I'll have to plug that into my spreadsheet and get back to you.

Post a Comment