I've noticed that the price of a 20 oz bottle of Gatorade can vary quite a lot within New York City. $1.00 in some places, up to $2.00 elsewhere. I don't drink enough Gatorade for this to make a huge difference in my own finances, but I can't help being curious about why this is the case. Is it just what they think people in that neighborhood will pay? Is it due to a beverage distributor that covers a particular neighborhood? Are prices marked up in areas where there are likely to be thirsty joggers? So I have decided to create a map showing the price of Gatorade at different locations. (NOTE: I will limit this to single-bottle purchases in delis, which are presumably independent and don't have the bulk purchase advantage that chain stores would have.) Who knows, perhaps my research will reveal some interesting trends! My initial data points are noted below:

(Now readers can follow my travels around New York City via my Gatorade consumption.)

Tuesday, August 30, 2005

NYC Gatorade Map

Labels:

food,

price comparison

![]()

What $2 Will Buy

In a restaurant in my neighborhood, one VEAL BRAINS taco.

But an order of Steamed Tongue costs $9.00.

Yuuummmm.

This is one takeout menu I'll be keeping right by the phone...

Labels:

food

![]()

Sunday, August 28, 2005

Time to Sell?

I think I'm going to sell my bond funds (CHTMX, MBDFX and HXBAX). The more I learn about how they are affected by rising interest rates, the more now seems like the time to do it. I think having these funds in my portfolio helped me out when the stock market wasn't doing as well, but I think they might be heading into a long term slide as interest rates increase, so their usefulness may be over. The share prices are down slightly from when I bought them, but my ROI is still in the black because of dividends paid, so I don't feel like I'm losing a ton of money from a panicked dump. But I definitely could have earned more from that $7000 over the past couple of years. Oh well, lesson learned.

This will only be the second time I've ever sold any of my investments. Some people seem to have the problem of selling too soon, perhaps I am just the opposite... BRSIX is up about 107% from when I bought, but I can't decide if I should take the money and run, or wait it out and hope it keeps going up.

Now I have to research some other funds to put that money in...

![]()

Friday, August 26, 2005

5K

I wish that title meant I was running a 5K race to raise money for some worthy cause. Unfortunately I can barely run 5 blocks, let alone whatever a K is, but the good news is that this blog got its 5000th hit sometime today! A big thank you to everyone who has been part of this, especially those who have commented or posted links back to the site. It hasn't even been two full months since I've started writing My Open Wallet, but I'm having a lot of fun with it, and I hope it's fun to read too.

As for the future, here's a few things I've got cooking:

--Some customization of the design, as I'm getting sick of the green.

--A series of articles about my financial genetics: influences from family members

--A look at what different people mean by "middle class"

--Some stories about childhood money-related experiences

--More details about various expense categories

--More scathing reviews of books I haven't read

--An X-rated tale involving Miracle Whip, 9-volt batteries, and Condoleezza Rice

So watch this space! And if there's anything else you'd like to see covered here, your dj takes requests so please let me know!

Thanks again,

Madame X

![]()

One is the Costliest Number

In today's New York Times, there was a story about people who live alone, with no immediate family to care for them. The article cited some interesting statistics about the number of single person households in the US:

Single person households as a percentage of all households:

1940-- 7.7%

1970-- 17.6%

1990-- 24.6%

2003-- 26.8%

There could be lots of reasons for this-- higher divorce rate, people marrying later, more societal acceptance of gay people, etc. The numbers include people who have never married, are divorced, or are widowed.

The main thing he article talked about was what these people do when they are sick or need help with something, and don't have family members to take care of them. Reading about this today was kind of a coincidence because I had to accompany one of my friends to a minor surgery, and pick up her prescriptions and make sure she was settled in at home to recover. I've done things like this before for another friend too. Among the women I know in NYC, there are a number of us who are either single or in long-distance relationships. We list each other as emergency contacts, help with things like putting in air conditioners or moving furniture, and have sets of spare keys to each other's apartments. But we would never dream of becoming roommates, because we all like living alone.

There must be thousands, if not millions of women like us in New York, and elsewhere, and it made me think about all the ways that being single is more expensive than being in a couple.

The one that comes most immediately to mind is housing, of course. For most of the time I've lived in New York, my income has been at a level where I could comfortably afford to share a one or two bedroom apartment, and in fact, since moving to NY I first shared a rental two bedroom in Manhattan, and then shared ownership of a 2+ bedroom in Brooklyn, both of them pretty nice and in good neighborhoods. Even now, despite the crazy increases in prices, I could still probably afford half of a two-bedroom apartment in Brooklyn, and definitely half of a one-bedroom. But if I compare my income over the years to the cost of renting a studio apartment, it's always been tight, and owning a studio, or at least a studio in a closer-in part of Brooklyn, has tended to hover a little above my reach. A studio in Manhattan, or a one-bedroom in Brooklyn, has always been pretty much impossible. Why does half of two not equal one when it comes to housing? Also worth considering: perhaps this demographic shift to more people living alone is part of the reason housing prices keep rising-- two people living alone need twice as many homes as two people living together, so it causes more demand.

Travel is another obvious issue--all those package tour deals you see advertised for outrageous prices are always based on double occupancy. I don't tend to travel alone or buy those package deals anyway, but it's just annoying to know that if I did, I'd have to pay a "single supplement" that would make it no longer such a bargain. And of course there is rarely any such thing as a single room in a hotel, and if there is, it's not that much cheaper than a double room. Again, half of two does not equal one.

Then there's things like car rental. If you rent a car and want two unrelated people to be authorized to drive it, you often have to pay an extra fee. Some years ago, my ex- and I discovered that at some companies, this fee would be waived for registered domestic partners, so we ran down to Borough Hall and got hitched! (OK, it didn't quite work like that, but it actually was one of the things that got us started thinking about tying some kind of knot, that in retrospect, shouldn't have been tied...)

And what about the bane of my financial existence, food! Well, of course it is very frustrating to go grocery shopping for one person. There is one supermarket in my neighborhood that I just can't go to because everything in the meat section seems to come in 8-packs for families. I don't even have a full-size fridge, where the hell am I going to put 7 extra pork chops?! And there are a lot of recipes that just aren't practical to try to cut down to single portions, so you have to be ready to eat the same thing a couple of nights in a row most of the time.

Don't get me wrong-- I love living alone. I have plenty of company when I need or want it, but I think I will always want to have my own space, no matter what sort of relationship I'm in. (My current partner and I often joke about buying a huge amount of land somewhere and living in two little cabins next door to each other. Which I'm sure will cost more than twice as much as one large cabin.) One does not have to be the loneliest number, but it is the most expensive.

.

![]()

Thursday, August 25, 2005

Rule #10: Make Enough Money

Doh!

- Make enough money to support your desired lifestyle

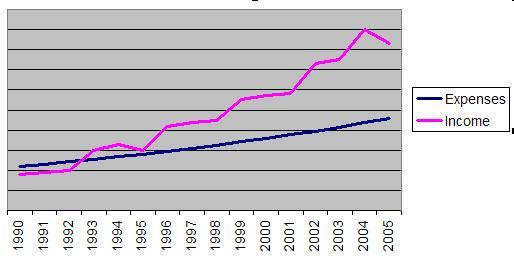

I'm not an extravagant big spender with super-luxurious tastes. There are a lot of things I do without. But like anyone else, I have certain minimum standards about how I want to live, and they don't seem to vary much. Here's an illustration:

This is not drawn with accurate figures, but represents a rough sketch of my financial history. The early years were tough, as I was not making much money while trying to live on my own for the first time. I didn't get into huge amounts of debt, but there were a couple of years where I must have barely broken even, if that. Then there were years when I saved a little, but not much. It's only more recently that my income has grown to a point where I could save a lot, but only because my spending hasn't ballooned to match.

This is not drawn with accurate figures, but represents a rough sketch of my financial history. The early years were tough, as I was not making much money while trying to live on my own for the first time. I didn't get into huge amounts of debt, but there were a couple of years where I must have barely broken even, if that. Then there were years when I saved a little, but not much. It's only more recently that my income has grown to a point where I could save a lot, but only because my spending hasn't ballooned to match.Unfortunately, it's not like you can just select the amount of money you want to make on a checklist when you are hired for a job! (I can fantasize about the HR paperwork: "Let's see, I think I'd like dental plan B, and I'll put $50 a month in a FSA, and hmmm, well, I'd like to be able to afford two homes, a yacht and an all-Prada wardrobe so I think I'll take the $400,000 to $449,999 salary range...check!")

But there are times when you have a choice in the matter. If you happen to have a passion for collecting Rolexes, a career as a social worker might not be the right choice for you! (From what I hear about social work salaries, even having a passion for 3 meals a day might be a problem...)

I may not be able to choose to make as much as I want, but I can choose to approach my career in a certain way and devote a certain amount of energy to it so I can move up the ladder and make more money. I can choose to pursue a job at a company or industry based on its average pay scale. Sometimes I choose not to follow the money, because other things are more important. Yes, grasshopper, as usual, it all comes down to balance.

Labels:

income,

living within one's means,

Rules,

salary

![]()

Wednesday, August 24, 2005

Rule #9: D.I.Y. vs P.A.Y.

Okay, this may be the wishy-washiest rule ever. But I guess I think of my rules more as philosophical cattle-prods than actual strict instructions.

- Don't pay someone else to do what you can easily do yourself

Here's a few other things where this part of the rule applies:

Do my own nails vs. going to a salon

Walk or take the subway instead of taking a taxi

Clean my own home instead of hiring someone else

Paint my own walls instead of hiring a professional

Buy unfinished furniture and stain & varnish it myself

All of these are things I don't mind doing and can do well.

But that brings up the flip side to this issue:

- Pay others to do anything that you might really f**k up!

Obviously, different people have different skills. If you are good at household renovations, of course you'll save lots of money doing them yourself. But if you're not so good, you may end up incurring extra costs, not to mention the potential for personal injury!

This relates to a recent post at The Happy Capitalist about garage doors and financial planning as do-it-yourself endeavors. He makes the great point that money management is an area where many people don't seek out professional help but probably should. I am an example of this, I think. I (hopefully) have enough basic financial knowledge not to do anything rampagingly stupid with my money, but I could probably get higher returns from my investments. Years ago I told myself I should see a financial planner, but the one whose name was given to me apparently worked on commissions rather than a fee, and the friend who used her felt like she'd been steered towards particular funds for biased reasons. I do pay an accountant to do my taxes--I started doing it when I owned a co-op and my deductions were more complicated. Now that I am renting, I could manage to do them myself, but I trust my accountant to do them better. I'm sure she's found me enough extra deductions over the years to more than repay her fees.

One other factor comes into this rule: time.

- If you can really make better use of the time, pay someone to do things that take up time

When do you DIY instead of PAY? Let's hear it, readers...

Tuesday, August 23, 2005

Long Term Goals

I'm really bad at long-term planning. Whenever people say "where do you want to be in 5 years" I don't tend to have a good answer. I'm still trying to figure out what I want to be when I grow up. When it comes to finances, I've had a vague long term goal about being able to "retire comfortably," whatever that means. But for the last few years I've gotten better at making short term goals-- I've been making net worth goals a part of my New Year's resolutions. (And these are the only resolutions I've really followed through on!) So after starting this blog and delving into the many other great sources of financial wisdom that are out there, I was inspired to run some numbers and think seriously about a long-term financial goal.

A lot of people focus on the goal of getting to $1,000,000 net worth. I guess it's as good a goal as any-- it's a nice round number. I played around with some estimates of my future earnings and expenses and came up with a goal of getting to $1,000,000 net worth by 2015. I think this is at least somewhat realistic. I tend to be fairly conservative and pessimistic in my expectations, short of assuming that an asteroid will hit New York. But if I can get another promotion or two, which I think I am well-positioined to be able to do, and if I can keep my current costs at a reasonable inflation level over the coming years, and continue to earn about what I've been averaging from savings and investments, I think it might work out. And if I revamp my portfolio and shift some money away from the funds that have been lagging, maybe I can do a little better.

However, even if I have $1 million by my mid- to late 40s, I'll still have to keep working until 2038 if I want to retire with any kind of decent income, as far as I can tell! $1 million isn't enough. But I never know what to think about the assumptions that go into these retirement income calculators-- inflation percentages, tax brackets, etc. And I always have to plug in a ridiculous number of years I'll be living off the retirement income. No one in my family ever seems to die before their mid- 90s! A friend of mine said I should consider myself fortunate to have a high likelihood of a long life, and I said, sure, that's all very well but how the hell am I going to pay for it?!

I'd love to know what goals other people have set, and how you calculated what you'd need for your retirement. And also, do you have an asteroid contingency plan?

![]()

Sunday, August 21, 2005

Real Estate Cost Analysis Tool

It's easy to find mortgage calculators online. But they are not always set up for New Yorkers, who tend to be buying co-ops, and I wanted to analyze the costs in more detail. I set up my own "rent vs. buy" housing cost calculator in Excel using these steps. I won't go into the details of the formulas-- you can download the spreadsheet to see them.

First I generated a payment table for the loan. This tells you the total payment, and how much is interest and how much is towards the principal, with variables for the term of the loan, interest rate, and amount.

I then incorporated this into another worksheet with information about my income, tax bracket, and other factors about the property I'd be buying: maintenance fees, tax deductibility of maintenance and utility costs. It's set up so you just enter the variables in the shaded boxes, and it references the results from the payment table. So it tells me how much I'll pay, before and after taxes, and what percentage of my gross income the payments are. But there are other factors I want to consider.

So it tells me how much I'll pay, before and after taxes, and what percentage of my gross income the payments are. But there are other factors I want to consider.

When people tell you why you should buy vs. rent, they always say it's because the money builds up equity instead of just going out the window. But there are still "out the window" costs when you buy: the non-tax-deductible part of your interest and maintenance payments. Right now, I pay $850 in rent, which all goes out the window. So am I saving more money if I buy an apartment and am building equity? Maybe. In the example in the screen shot, even after you account for equity and tax deductions, my out the window costs are actually higher if I buy this apartment. That might be okay up to a point, (and of course equity also builds up by the value of the property increasing ) but it's something I want to be aware of. I have to really believe it's worth it to have that much more money go out the window every month, which is on the spreadsheet as "non-equity costs."

Then I have to see how the cost of ownership matches up to my paycheck and other expenses. Will I still be able to meet savings goals if I buy? Will I be able to maintain my current lifestyle? I added a simplified budget of expenses that come out of my paycheck cash. (To keep things easy, I left out taxes and payroll deduction items.) I'm not willing to go into the red every month, even knowing that I'll get some of the money back as a tax refund.

I made a "NOW" and "IF I BUY" column, so I could adjust for the raise I should be getting soon, and cutbacks I'll try to make in spending. "NOW" is averaged out based on the past year's expenses. I then take the monthly expense averages vs paycheck cash, tax refund and bonus, and calculate a year end net.

I also added a savings goal section. I set this up as a goal that would include the equity I'd be building, as well as cash-only savings below. These don't include my 401k,or interest/investment income that goes into savings. Then it all comes together here:

Then it all comes together here:

It tells me how much I'm spending and saving, and if I can't meet my savings goals, it tells me "NO!!" I also added a calculation that would tell me if I am breaking even with my current savings level if I include the equity build-up.

Here's a different example of a scenario that would actually be affordable for me-- if I'm meeting my savings goal, the pink box says "OK":

I think the usual guidelines-- that you should pay 30% of your income towards housing, or that you can qualify for a mortgage that is 2.5 times your gross salary-- are too broad. They just don't take into account the reality of people's lives and their real goals. I had fun putting this calculator together and playing around with the different scenarios. It puts things in a different perspective when you see how a change in one part of your spending can affect your ability to buy a home. I'm sure the worksheet could be made prettier and other bells and whistles could be added, but if you want to use it as it is, or just check it out and make comments or improvements, you can download it here.

Labels:

excel charts,

real estate

![]()

Friday, August 19, 2005

Luxembourg et Veritas: More on The Millionaire Next Door

Ok, I felt like I may have been a little harsh the other day. Another thing I DO like about The Millionaire Next Door: his formula for determining whether you're a PAW (Punk-Ass Whitedude? No, Prodigious Accumulator of Wealth.) All Things Financial has a good summary of it here. This formula helps clarify the very good point that it's not all about having a million dollars, it is about when in your life you have it, in relation to your yearly income. If you have $1 million in net worth a year before you retire at 65, and your yearly income is over $160k, you're not really considered "wealthy," or at least not a good accumulator of wealth. Basically, he's saying that if you make that much money a year, you have no excuse for not having saved more. But according to the formula, if you're 64 and you only make $70,000 a year, you are to be congratulated for what you have achieved by even getting to half a million. (But though you are good at accumulating wealth, you're not wealthy. If you're trying to retire on half a million, you'd better keep pinching your pennies, or hope you don't live too long! I'm not sure the formula makes as much sense when applied to older ages.)

But back to the stastistical silliness. In that list of smaller ethnic groups represented among millionaires, I noticed the curious presence of "Luxembourger." This really has to win the prize for great crashing irrelevance. Based on his sample size of about a thousand millionaires, I'm guessing maybe one of them came from Luxembourg. But does the lucrativity of this lucky Luxembourger support the author's theory that these small, recently arrived ethnic groups haven't yet "become fully socialized to our high-consumption lifestyle" and that's why they are well represented among high accumulators of wealth? Not likely: Luxembourg is one of the tiniest, wealthiest countries in the world.

Some information about Luxembourg from the CIA World Factbook:

Population: 468,571 (no, I didn't leave out any zeros. It's about as many people as live in New Orleans, or .007% of the world's population.)

Size: approximately 998 square miles. Smaller than Rhode Island.

GDP per capita: $58,900, which is about 47% higher than in the United States.

Quote: "The country enjoys an extraordinarily high standard of living."

Isn't it heartwarming to think of all those tired, poor, huddled masses of Luxembourgers coming to America to breathe free and become millionaires...

Labels:

books

![]()

Thursday, August 18, 2005

Cheap and Free Fun

A commenter asked about what I do for fun, and how to do it cheaply. Here are a few suggestions:

Gym: I haven't researched the cheapest gyms in the city, but I think the YMCA is a pretty good deal. Other ideas: in the summer, all the outdoor city pools are free. Most offer dedicated times for adult lap swimming in the early morning, and some in Manhattan also have times in the evening. You can also join the city recreation centers that have indoor pools for only $75 a year.

Free kayaking: Head to Pier 26 on the West side for the Downtown Boathouse free kayaking. It's fun to paddle around and get a different view of the city. Just don't expect to go too far, as you have to stay within an enclosed area.

Staten Island Ferry: it's free, and a great way to cool off out on the water. You get wonderful views of lower Manhattan and the Statue of Liberty.

Battery Park City: there are free ping pong and pool tables in one of the parks along the river, and in general it's a nice place to hang out.

Foreign language lessons: Again, I haven't researched all the options but I know the Alliance Française (French) and the Instituto Cervantes (Spanish) offer classes and can help you find a private tutor. See if other people at your office would be interested in sharing a small class during lunchtime. Baruch College also had reasonably priced classes last time I checked. See if your employer offers tuition reimbursement. Also, check out Craigslist for people who would swap conversation practice. Sometimes conversation groups also meet in bookstores such as Barnes & Noble.

There are millions of other fun things to do for free, here in New York and in other cities-- check out TimeOutNY magazine, or whatever paper has the local listings.

But if all else fails:

Get drunk, get naked, and vacuum.

Labels:

free stuff

![]()

Basketball

I went to a NY Liberty game the other night. Unfortunately, I did not get to see this particular match-up of players! But I did manage to spend $20 for a ticket (for a seat that normally costs $45 for season ticket holders or $54.50 full price) and about $40 for food for 3 people. Yes, they charge $6 for a can of beer at Madison Square Garden. Welcome to New York.

I went to a NY Liberty game the other night. Unfortunately, I did not get to see this particular match-up of players! But I did manage to spend $20 for a ticket (for a seat that normally costs $45 for season ticket holders or $54.50 full price) and about $40 for food for 3 people. Yes, they charge $6 for a can of beer at Madison Square Garden. Welcome to New York.

But the good news is that you get an enormous amount of food when you order the $6.25 chicken fingers. So I brought home leftovers! Who the hell brings home leftovers from a basketball game, you're thinking. Madame X does.

![]()

Wednesday, August 17, 2005

Free Inflation Calculator for Palm PDAs

There is a fun and free piece of software for Palm devices that allows you to enter an amount and any two years between 1800 to 2005 and see the effect of inflation. For instance, my $79,000 salary today is the equivalent of earning $3,427 in 1900!

Labels:

free stuff

![]()

Tuesday, August 16, 2005

Mini-rant

Why is iced coffee so much more expensive than hot coffee? It's been so roastingly hot in New York the last few days that I've been buying iced coffee in the morning, which costs 64 cents more for a small. Are a few ice cubes really worth 64 cents? See, this is why global warming is a problem-- if NYC was this hot all year round, it would cost me an extra $160 a year for my morning coffee. Actually probably even more, as they'd raise the price of ice due to increased demand. In fact, the entire economy of NYC could be thrown off by then, as the whole city will probably be underwater.

Yes, I know I should just be brewing a pot at home, keeping it in the fridge and taking it to work in a travel cup.

![]()

What I Spent...

8/1 to 8/15:

Cash: $242.62

--$14.00 laundry & drycleaning

--$5.00 taxi

--$1.00 Wall Street Journal

--$20.00 loan to friend

--$202.62 food/dining

Credit card: $431.05

--$7.73 gift given

--$9.99 book for French class

--$43.00 train tickets

--$27.52 drugstore

--$23.90 AOL

--$318.91 food/dining

Checking: $874.49

--$24.49 telephone

--$850.00 rent

Labels:

spending

![]()

Monday, August 15, 2005

Flexible spending account

I try to take advantage of any tax break I can, so the last few years, I've signed up for my company's healthcare flexible spending account. Last year I think I had them deduct $500, and on Dec. 28th I was scrambling to spend the last $150 or so. (Prescription sunglasses did the trick-- what I really needed was regular glasses, but I couldn't find frames I liked.)

So this year, I decided to contribute less. But guess what, I was sick a lot over the winter, and here it is, only August and I was just about to submit a claim for the everyday eyeglasses I finally did find, and the accompanying eye exam, when I discovered that I've already maxed out my reimbursements, and I should have contributed about $350 more than I did.

I'd rather have a FSA than nothing, but it really is a pretty stupid solution to a larger problem. How are you supposed to predict when you'll get sick?

![]()

Sunday, August 14, 2005

What Color is Your Millionaire?

Considering that I think a lot about personal finance, and bother to write a blog about it, you would think I had more interest in reading books about the topic. I like reading books about larger economic issues, such as The Lexus and the Olive Tree and The World is Flat, both by Thomas Friedman. And books with demographic information, such as Who We Are Now, or about the lifestyles of different social classes, such as The Working Poor and Bobos in Paradise, fascinate me.

But I don't read much from the personal finance section. I browse books about investing, as I know I have a lot to learn in that area, and sometimes I will flip through books like The Automatic Millionaire if I'm in an airport, but otherwise, I tend to avoid this category. However, I'd heard a lot about The Millionaire Next Door, and thought it might be interesting, so when I had some time to kill the other day, I parked myself in a corner of the local B&N, and started to look through it. But I was only a few pages in when I got really annoyed.

First of all, his data is pretty bogus, as other critics have pointed out. His methods can't be called statistically accurate. But what really pissed me off was the section called "You or Your Ancestors." He's trying to say that no, you don't have to be a Mayflower descendant to be a millionaire, and that not everyone who is wealthy inherited their wealth rather than building it themselves. "America continues to hold great prospects for those who wish to accumulate wealth in one generation," he says. Well, that is all very inspiring but then he proceeds to chart the ethnic makeup of his millionaires vs. the percentage of these ethnic groups in the U.S. population. The #1 group are people of English ancestry, at about 21% of millionaires vs. 10 % of the population. Then you've got Germans, Irish, Scottish, Russian, Italian, French, Dutch, Native American, and Hungarian. If you look at it another way, people of 9 European ancestries are 80.4% of millionaires vs. only being 51.6% of the population.

Doesn't that begin to sound like opportunity might not be so equal for all?!? I mean, hello, this is not the 1800s anymore! If an Irish person becomes a millionaire that can hardly be trumpeted as an example of our equal opportunity society allowing an opressed minority to triumph over adversity. He makes no mention of African-Americans, Asians, or Hispanics as even existing, let alone their representation among millionaires. As for the Native Americans he mentions, I think that is an example of his skewed data. Maybe they slipped in because he was trawling for survey participants at casinos. I just find it anomalous that this is the only minority group that makes it onto his list, and it is at odds with other statistics that I've read about the income levels of Native Americans.

The author also lists a chart of ethnic groups that tend to be more recent immigrants and who make up very small percentages of the population but have higher than usual wealth levels-- I found it rather disturbing that he seems to go out of his way to highlight the position of Israelis on this list, as if to confirm anti-Semitic stereotypes about Jews & money.

Of course I am not trying to do a full book review here-- I admit I've only read a small part of it. I do think that the main point of this book, that you are more likely to be wealthy if you don't flash expensive status symbol possessions all over the place, is a valuable message for many people to hear. But I felt like the book should have been titled "The White Millionaire Next Door" or "Some Millionaires that Live Next Door to People I Know," or "Some of My Best Friends are Black but Of Course None of Them Live Next Door or are Millionaires."

I realize that the point of this book is not to critique race relations in America. We do live in a society that at least theoretically offers equal opportunity, and people of all colors, religions and backgrounds can and do become millionaires. But there is also blatant, persistent inequality between the races when it comes to income levels and net worth-- just look at the census data. To indulge in Panglossian gushing about how great it is that we can all become millionaires, and not acknowledge reality is offensive, and just stupid in a book that claims to have some basis in research. Not to mention that the author has obviously just forgotten that something like 30% of his potential readers don't happen to be white.

Friday, August 12, 2005

Real Estate Tracking

I've been tracking how many homes are listed for sale on the NY Times website over the last couple of months, for both Manhattan and Brooklyn. This is my somewhat lame way of trying to see if my bubble-bursting tactics are paying off (god, I am so sick of lugging that tuba around!)

Well, I can't say I'm seeing results. The number of places for sale doesn't seem to have ballooned at all. It's pretty much stayed flat, with slight increases and decreases week to week.

Of course, I am only tracking the NYT ads. There could be plenty of places for sale that are not advertised there. They may only have a limited number of ad listings. Real estate agents might not advertise too many places, to give the impression of a tighter market. There are a million reasons why this is not statistically valid.

Oh well. Last night I sat around with a friend and talked about how much apartment I could afford if I suddenly got a $50,000 raise. Probably a nice one-bedroom or smallish two bedroom in Brooklyn, woo-hoo!

Labels:

real estate

![]()

Thursday, August 11, 2005

Rule #8: Work for free...

Free stuff, that is!

- Work where you get something you love for free.

I do not work in a high-paying industry. 15 years into my career, I probably still make less than most first-year law firm associates, and I think I've had a better than average, if not stellar career path compared to other people in publishing. But I've always had a few perks that made it worthwhile. I don't mean perks like free espresso and ping pong tables in the office. One of mine is books: I've always loved to read, which is why I was drawn to publishing in the first place. If I'd had to buy all my books at full price, I'd be many thousands of dollars poorer. The other big perk I've had has been travel. At one of my jobs, I had to go to Europe 3 or 4 times a year, and was usually able to extend my trips into at least a few days of vacation time. I also racked up a lot of frequent flier miles than I was able to use for personal travel, again saving me thousands of dollars. I also save money in other small ways because of my job. I occasionally get free meals. And when it comes to tax time, I can deduct everything under the sun: internet access, movies, plays, museums, magazines-- all of these things very legitimately contribute to my awareness of the book market!

I'm sure I could also have been happy working in some other career where I made more money (and had the espresso and ping pong), but I'm sure there are many paths I could have taken that would have made me miserable. I kind of stumbled into what I do, but I've always felt that it is a pretty good balance in terms of its challenges, its time demands, and its benefits.

Labels:

books,

career,

free stuff,

Rules,

salary

![]()

Wednesday, August 10, 2005

More stuff to spend money on!

Just discovered this site: Strange New Products

There is some funny stuff on there!

Labels:

spending

![]()

Things I could be doing to save money

I'm a fairly frugal person in many ways, but there are a lot of things I could be doing to save money that I am not. Here are a few:

- Email more instead of phone calls-- this is reasonable, I should do it, though sometimes you do need to just talk to people.

- Read newspaper online instead of suscribing-- impossible to do on the subway, so no dice.

- Never eat out, buy cheaper groceries-- I'm working on making improvements in this area, it's definitely where I have the most to gain! I've spent almost $400 on food already this month and it's only the 10th!!

- Never buy even used books, go to library more often-- this wouldn't actually save me that much money, I spend less than $100 a year on books because I can get a lot for free anyway.

- Make gifts instead of buying them-- hmm, hope everyone liked the beaded necklaces and painted picture frames they got last year... and the year before...

- Take bus instead of train or flying for family visits-- ugh, the bus is something I'd like to think of as a distant memory from my younger days.

- Never travel-- no way

- Never take classes-- no fun

- Never take taxis-- I only spent about $250 on personal taxi use last year, most of which were trips from the airport. If I am coming home late at night, with luggage, I think it's worth it. I almost never take shorter trips within the city. And I take the Airtrain and subway whenever I can.

- Clothes: always on sale or thrift shops or not at all-- I spend about $2-3000 a year on clothes because I have to (and want to) look relatively professional-- I've always tried to follow the rule of dressing for your next step up the career ladder. I try to buy good things that will last, not a lot of trendy crap. I'd rather have one good pair of shoes that cost $300 than 15 pairs of flip-flops that would make me look like a beach-comber at the office. I think this is probably a good investment. I'm sure I could be a little more bargain conscious, but I do try to find things on sale. I don't find thrift shops to be worth the time it takes to pick through the junk.

- CDs: borrow from library and burn into itunes-- I haven't been spending too much on music lately, but I haven't checked out what the library has... could be worthwhile.

- No new housewares-- I'm mostly sticking to this one, at least until I buy an apartment.

- Live with a roommate-- I'm not sure this would actually be much cheaper than my current rent, at least in my same neighborhood. And when you hear people's horror stories about roommates running up bills and trashing places, I think I'm better off knowing that the only person responsible for the bills is me.

Tuesday, August 09, 2005

From the clipping files...

Here's a few items of note:

People whose net worth is over $70,000, the median in the United States, are 30 percent less likely than poorer people to feel pain at the end of their lives, according to the Journal of Palliative Medicine.

Teenagers today may be better prepared for retirement than previous generations. According to Kiplinger's magazine, 3 out of 4 teenagers have a part-time job during the school year. More than half are saving for college, and of those who own stock, 32% said they had bought it with their own money.

According to the National Association of Realtors, (their website has lots of interesting data) the housing affordability index dropped sharply in Q2 2005, even as sales of existing homes hit a record level. The median family income level was $56,917, which is supposed to be enough to cover a house costing $251,900, and the median price for homes was $208,500. This is not very comforting to me, as the median income level in my neighborhood is only about $51,000, and yet studio apartments are hard to find for under $250,000... and I also believe that the definition of "affordability" in these studies can be sort of wacky. I don't believe that a home is affordable if I have to live on ramen noodles in order to pay for it!

![]()

Monday, August 08, 2005

Jury Duty

What a drag. To approach this in a somewhat on-topic way, let's look at the fact that jurors are paid $40 for an 8-hour day. Isn't that less than minimum wage? They should pay you extra for the sheer mind-numbingness of the experience.

The most interesting part was the sadistic Filipino guy who was in my group as we were being interviewed by the attorneys. I say sadistic because he seemed to take great pleasure in telling one of the other prospective jurors that in his country, when he was young, he was told that "if you want to keeeel someone [said with his eyes opened very wide] you have to ask yourself if you have enough money to pay for the lawyers, and if you can pay to keep yourself out of jail, then go ahead and keeeel the person." He also let slip that he was only "there for a friend"-- hey, no photo ID required! And he mentioned that during lunch break, he'd spoken to Fernando Ferrer, a mayoral candidate here, and told him "he will never weeen because he is running against a beeellionaire!"

Friday, August 05, 2005

A Day Off...

It's nice to take a day off during the week and do errands around the neighborhood. You see things in a whole different light, and realize that the pizza man knows everybody, especially the old ladies. (Slice of pizza and small Diet Coke: $2.35)

One of my errands was going to the Salvation Army to donate some clothes that I don't wear, and a few other odds and ends. I love getting rid of clutter, and in an apartment the size of mine, you don't really have a choice. I also went to the local used bookstore and traded in some books for credit towards other ones.

Now maybe I'll go to the beach!

![]()

Rule #6: Max out your 401k and Roth IRA

- Contribute the maximum allowed amount to your 401k and Roth IRA every year.

I started this with my first job and I'm so glad I did. I decided it would hurt less if I just started out my working life without having that money in my check, as opposed to making the decision to start taking it out later. I like being forced to save money-- I am not so disciplined that I don't need this kind of help! And of course it is great that it is deducted before taxes, and my employer matches a portion of my contributions too.

The Roth IRA was a little harder, since I had to make myself set it up! There were a couple of years where I didn't get around to it, but I have 6 years' worth of maximum contributions now. The first couple were CDs at my local bank, which involved going in and talking to someone at the bank who wasn't very helpful. But now I have an E*Trade Roth IRA account, so for the last few years it's been easy to just transfer the money in, and I've been putting it into mutual funds that will hopefully earn more than CDs in the long run.

Retirement is such a tricky subject. According to the calculator in Quicken, if I continue at this pace, I should at least be able to retire in my early 70s without starving to death. But that assumes a lot of variables that I’m just not sure about: what will my tax rate be when I retire? How old will I be when I retire, and how long will I live after that? Crystal ball, anyone?

Labels:

retirement,

Rules,

saving

![]()

Thursday, August 04, 2005

Rule #7: The Now or Later Rule

Many people will tell you that before you spend a dollar, you should think about the future value of that dollar if you invest it. The thinking is that if you save money now, it will grow via investments, and then someday you'll have more money to do the things you want to do, and presumably, more time to do them when you're retired. This is not bad advice. I expect to live until I'm well into my 90s based on my family history, and I want to have resources to enjoy that part of my life.

But on the other hand, you can't save everything for a rainy day. Sometimes I ask myself this question:

- If I don't buy/do this now, will I still be able to enjoy what I'm buying/doing later?

Having a big house: postpone it, I can enjoy that when I'm retired

Elegant furniture: postpone it until I'm old and need to spend a lot of time sitting down or in bed

A car: postpone it, I'll have more of a need for it later, at least until I start to really lose my faculties, or get osteoporosis and turn into one of those little old ladies who can’t see over the steering wheel.

Travel: hmm, I might not enjoy mountain hikes and swimming with wild dolphins when I'm arthritic and decrepit. Better do it now.

Sailing: again, I might not be physically able to do it later, so I should do it now.

Gym membership: there may be cheaper ways to stay fit but if I even want to make it to old age, I don't think I should skimp on exercising.

Education: sure, do it now because it's an investment in the future anyway and I might have Alzheimer's later.

Clothes: who knows, maybe when I'm 80 I'll be rocking Miu Miu instead of muu-muu, but I think it's a better bet to enjoy wearing nice clothes now while I'm still young and slender!

I certainly don't make all my decisions using the "a bus could run over me tomorrow" argument: I do think you should plan for the rainy day. But I also think you should make hay while the sun shines, or at least before your knees give out.

Labels:

clothes,

decisions,

frugality,

living within one's means,

Rules,

self-image,

travel

![]()

Wednesday, August 03, 2005

How I Did It

A commenter asked how I have managed to save the money I have. Here are a couple of short answers:

- I started contributing to a 401k as soon as I could, and have always contributed the maximum level. I've also opened Roth IRAs.

- During maybe half of the years I've been working, part of my compensation has been in a bonus, anywhere from $1000 to $25,000 a year, (which was sometimes as much as half my total yearly earnings paid in one lump sum). I've always tried to put most of it straight into savings.

- With my first big bonuses going to the downpayment, I bought a home with a partner at a fairly young age (mid-20s). It was right before real estate prices started going through the roof-- the best timing I've ever had. When I moved out and was bought out, my share of the equity was $50,000, (a return on investment of about 500%!) which went straight into savings and investments. (Of course I should have put it straight into another apartment...)

- As for where I live now, I was lucky enough to find a cheap but very small apartment that most people might not be willing to live in just because of the size, though it's actually rather cute and gets great light.

- And basically, I've just kept my lifestyle in line. From when I first started working, I tried to keep my spending lower than my earnings. It was hard at first, but as my income has grown through a few job changes, I've kept my level of spending roughly the same. And if I earned a lot more, I would still probably live in a similar way. I don't feel deprived-- of course there are things I would like to have someday that I don't have now, and I can have my envious moments when I see how other people live, but for the most part, I feel like my life is pretty good.

Tuesday, August 02, 2005

What happened?

Weird, my last post disappeared, and so did some recent comments... anyone else having Blogger problems?

![]()

Monday, August 01, 2005

The absolute worst thing to spend money on...

...is this.

Though it did occur to me that it might be fun to sneak into a ritzy country club and hang them on some elderly socialite's Cadillac...

Labels:

best don't-buys,

fun,

spending

![]()

H2Oh No!

I recently posted about how I try not to spend money on bottled water. In today's NY Times, there was an article with even more compelling reasons not to! Here's a few key points:

- Most people can't tell the difference between bottled water and tap water in blind taste tests.

- In 2004, Americans drank on average 24 gallons of bottled water

- This year, Americans will spend $9.8 billion on bottled water.

- Ounce for ounce, bottle water costs more than gasoline. It costs 250- to 10,000 times more than tap water.

- There is no health or nutritional benefit to drinking bottled water: in fact bottled water can have higher levels of bacteria than tap water, and it isn't subject to as much regulation and monitoring.

- If you are trying to avoid chemicals that can be present in tap water, you're out of luck: they are in some bottled water anyway, and also, unless you are wearning a gas mask while showering and unloading your dish washer, you're being exposed to those chemicals anyway.

- Bottled water is bad for the environment, due to shipping, refrigeration and bottles going into landfills.

- More than 1 billion people lack access to safe drinking water, leading to illness and a lack of productivity and a dependence on foreign aid in many parts of the developing world

- Clean water could be provided to everyone on earth for an outlay of $1.7 billion a year beyond current spending on water projects.

The author of this article wrote a book that has been on my list of things to read someday: A History of the World in Six Glasses, by Tom Standage. It talks about the role that these six drinks have played in world history: beer, wine, spirits, coffee, tea, and cola drinks.

![]()